Meet Complyport at the iFX Expo International 2026

We are excited to share that Complyport will be exhibiting at the iFX Expo International at Booth 109. Visitors can meet our regulatory, compliance and technology specialists and discuss the challenges and opportunities facing financial services firms in a rapidly evolving regulatory environment. With decades of industry experience, Complyport combines practitioner-led consulting with specialist RegTech capabilities to help firms manage regulatory complexity in a practical and scalable way. Our approach is designed to support firms across licensing, governance, risk, compliance, reporting and operational resilience, helping turn regulatory obligations into better oversight, stronger processes and more informed decision-making. At the event, visitors will be able to learn more about Complyport’s technology solutions, including: MAP FinTech: Regulatory Reporting & Trade Surveillance ComplyPortal: GRC Platform ViCA: GRC Agentic AI Platform COMPDEFAI: Cybersecurity & Resilience CAPTURE: Seized Asset Management Platform UnifyInsure: Insurance Technology Compliance and Learning Solution: GRC eLearning Visitors to the stand can explore how these solutions support firms with regulatory reporting, trade surveillance, governance, risk and compliance workflows, cybersecurity and resilience readiness, AI-supported compliance operations, digital insurance processes, compliance learning, and seized asset management. We look forward to meeting clients, partners and industry professionals in Limassol, exchanging views on the issues shaping financial services, and discussing how Complyport can support firms with both advisory expertise and technology-led solutions. To arrange a meeting with our team during the event, please get in touch in advance or visit us at Booth 109. See you in Limassol!

Complaints Handling: The Risks of Manual Processes

In an era where customer expectations are higher than ever, effective complaints management has become a critical business function rather than simply a regulatory obligation. Yet many organisations still rely on manual processes that can be slow, inconsistent, and vulnerable to human error. This not only risks customer dissatisfaction but also exposes firms to increased operational, regulatory, and reputational risk. The challenges of manual complaints handling start with the sheer volume of complaints that many firms receive. Each complaint needs to be logged, categorised, investigated, and resolved within appropriate timeframes. When these activities depend heavily on spreadsheets, emails, and manual workflows, inefficiencies quickly emerge. Delays, inconsistent handling, limited oversight, and missed actions can all undermine the customer experience and expose organisations to unnecessary risk. The human element adds another layer of complexity. Manual processes rely heavily on the judgement and experience of individual staff members. While this can be valuable, it also introduces inconsistencies. Different staff members might handle similar complaints in different ways, leading to inconsistent outcomes for customers. This can create a sense of unfairness and frustration among customers, as well as within the complaints handling team itself. The regulatory landscape adds further pressure. The FCA, for instance, expects firms to handle complaints fairly, consistently, and in a timely manner. Firms are required to have clear processes in place, to keep customers informed about the progress of their complaints, and to report complaint data to the regulator. Firms that can’t demonstrate effective complaints handling risk enforcement action, which can include fines and requirements to pay compensation to affected customers. But the business case for effective complaints handling goes beyond regulatory compliance. Firms that handle complaints well have an opportunity to turn a negative experience into a positive one, building customer loyalty and enhancing their reputation. Conversely, firms that handle complaints poorly risk damaging their reputation and losing customers to competitors. How ComplyPortal Can Help ComplyPortal’s Compliance Management System transforms complaints handling from a reactive to a proactive process. Customisable workflows ensure that complaints are logged, categorised, and resolved consistently. The document management system maintains a secure repository for all complaint records, making it easy to track trends and identify recurring issues. Task assignments and deadlines help ensure that complaints are handled promptly and fairly, while the audit trail provides evidence of compliance to regulators. Contact us for more information on how ComplyPortal can transform your compliance processes.

Policy Updates: How technology can support efforts to keep staff informed

Policies reduce risk only when people can easily access the latest version, understand what has changed, and apply it consistently. In many organisations the challenge is less about writing policies and more about keeping them current, distributing updates to the right audiences, and evidencing that staff have engaged with them. Updates can also be slow to coordinate, and lessons from incidents or staff questions do not always feed back into improving the policy. Technology helps by turning policy management into a controlled, trackable process rather than a set of documents spread across email, shared drives and intranet pages. Compliance management tools (often referred to as GRC tools) are designed to support this end-to-end. 1) How compliance management tools help A compliance management tool provides a central policy library that acts as a single source of truth. Policies can be clearly labelled with key information such as the owner, effective date and next review date, making it easier for staff to find what applies to them. These tools also strengthen control over change. Version histories and change notes help staff and management understand what has been updated and why, while archived copies make it easier to evidence what was in place at a particular time. To prevent policies drifting out of date, many tools support scheduled review cycles, automated reminders and escalation where reviews are overdue. This helps organisations move from informal periodic reviews to a consistent routine. They also support accountability by recording staff acknowledgements in a structured way. Rather than chasing replies manually, firms can track who has confirmed they have read and understood an update and follow up where responses are missing. Reporting and dashboards give management visibility of completion rates, overdue actions and recurring problem areas, allowing issues to be addressed before they develop into incidents. 2) How technology drives accountability Technology makes ownership clearer by assigning named owners and approval steps, reduces reliance on informal follow-up by making progress measurable, and highlights exceptions so they can be managed consistently. This also supports fairness, because expectations are clearer and staff can be directed to the correct, current content. 3) Good practice for effective use Firms get most value when policies are written clearly and kept practical, each update includes a short summary of what changed, and communications are targeted to the roles affected. Using reporting to prompt follow-up conversations, rather than focusing only on completion metrics, also improves outcomes. Staff questions and incidents should be treated as signals to refine policy wording, guidance and training. 4) What technology cannot do on its own Compliance tools support governance, but they do not fix unclear policies, replace leadership reinforcement, or solve cultural issues such as reluctance to raise concerns. They are most effective when paired with clear ownership, good drafting and active management oversight. Conclusion Technology helps organisations keep staff accountable and up to date by providing a single source of truth, improving control over policy changes, supporting timely reviews, and creating reliable evidence that updates were communicated and acknowledged. With modern technology now more accessible, secure and capable than ever, this is an ideal time to embed these solutions into day-to-day best practices rather than relying on manual workarounds. Used well, compliance management tools shift policy updates from a document exercise to an operational control that supports consistent behaviour. How ComplyPortal Can Help Embedding compliance into business operations is most effectively done through the utilisation of technology. A digital compliance platform makes it easy for all staff to stay aligned, enabling timely reporting and smooth internal communication. Here are just a few ways in which ComplyPortal’s Compliance Monitoring and Learning Solution by Complyport can support your firm’s compliance journey in relation to policy management: Centralised Documentation and Reporting: via secure, cloud-based systems, with the capacity to manage access control, internally, across teams. This can be utilised to store all relevant Manuals and Policy Documents for your firm, including AI Policies, UK GDPR, and Compliance Manuals. Monitoring: Allowing you to test for the effectiveness of your compliance program and detect potential compliance issues before they escalate. This reduces the risk of costly fines or penalties. Custom Reports and Audit Trails: Generate and export custom reports to suit your firms’ needs and the expectations of the regulator, with transparent and easy to export audit trails. Risk Assessment: the ability to map and address potential vulnerabilities, using our Risk module. Regulatory Updates: ComplyPortal notifies and tracks staff acknowledgements when there are important updates to policies and procedures. Contact us for more information on how ComplyPortal can transform your compliance processes.

Navigating Transaction Reporting: Choosing the Right Approach for Regulatory Compliance

Transaction reporting has evolved into a high-stakes pillar of regulatory compliance. Globally, regulators, including the FCA, ESMA, and ASIC, are increasingly focusing on the accuracy, completeness, and timeliness of trade and transaction reporting under various regimes, such as MiFID and EMIR. Failures can result in significant fines, reputational harm, and remediation costs. Firms today face additional complexity as they must report across multiple asset classes, jurisdictions, and regimes, each with its own technical formats, field definitions, and quality expectations. Regulators are no longer content with “best-effort” reporting; they require high data quality, consistency, and demonstrable controls. In this landscape, market participants generally adopt one of three approaches: 1. Delegated Reporting Under delegated reporting, the firm enters into an agreement with a broker, clearing venue, or intermediary that assumes responsibility for submission of trade reports to regulators on the firm’s behalf. Benefits Simplifies Execution: The client firm can rely on the intermediary to produce and transmit reports without building in-house infrastructure. Lower Initial Investment: Fewer internal resources are needed for reporting technology and staffing. Drawbacks Limited Control: The firm hands over control of report generation and quality, potentially masking errors or omissions until after submission. Accountability Remains with the Firm: Despite delegation, the firm retains ultimate responsibility for the accuracy and completeness of data, and the effort required for reconciliation can quickly outweigh the benefits of delegation. Regulatory Data Quality Considerations Regulators are increasingly focused on data quality dashboards, completeness checks, and audit trails. Delegated arrangements can obscure a firm’s ability to demonstrate robust controls or answer requests for evidence, elevating compliance risk. 2. Self-Reporting In a self-reporting model, the firm builds and operates its own reporting engine. This may be a proprietary solution or an internal compliance team producing reporting data to the regulator or competent authority. Benefits Control: Firms define and manage the full reporting process, enabling tighter governance and internal validation. Transparency: Full visibility into data transformations, field mappings, and submission logs improves auditability. Better Data Quality Management: Internal teams can implement robust checks, remediation workflows, and root cause analysis. Drawbacks High Upfront Costs: Developing and maintaining technology, hiring skilled personnel, and staying current with evolving rules demands investment. Human Resource Dependency: Requires ongoing reliance on specialised regulatory and data expertise, creating pressure on internal teams and increasing key-person risk. Regulatory Data Quality Considerations Self-reporting generally aligns well with regulators’ expectations for data quality and control frameworks, provided the firm invests in robust exception handling, reconciliation, ongoing staff training, and monitoring capabilities. Regulators value firms that can demonstrate end-to-end ownership. 3. Automated Reporting via Third-Party Vendor In this model, firms leverage specialised technology providers to manage the end-to-end transaction reporting process. r. Data is extracted from internal sources, validated and enriched, then transformed into the required regulatory formats before being submitted to the regulator or competent authority. Benefits Scalability: Vendors offer modular, adaptable platforms that can handle multi-jurisdiction and multi-product reporting. Continuous Updates: Vendors invest in compliance updates, technical specifications, format changes, and connectivity. Data Quality Tools: Many vendors include automated validation rules, deduplication, enrichment, and reconciliation engines. Cost Predictability: Licensing and service fees can be lower than building and maintaining comparable in-house capabilities. Shared Expertise: Access to vendor regulatory specialists helps interpret subtle regime changes. Drawbacks Dependency on Vendor: Selecting a vendor can be a time consuming process to ensure quality service and support. Integration Complexity: Initial onboarding requires technical resources and access to systems. Data Privacy / Security: Reliance on external systems necessitates strong controls around sensitive trade data. Regulatory Data Quality Considerations Vendors can help firms align with best practices through pre-built validation profiles, dashboards, audit logs, and governance frameworks. However, regulatory responsibility remains with the reporting entity, meaning firms must validate the vendor’s output through internal controls and periodic testing. Which Approach Is Best? Firms must evaluate their size, product complexity, risk appetite, compliance maturity, and budget. However, under the lens of today’s heightened regulatory focus on data quality and cross-regime reporting, some general guidance can be offered: Best for Small / Less Complex Firms Delegated Reporting may suffice where transaction volumes are modest, reporting requirements are narrow, and resources to build internal capabilities are limited. However, such firms should still implement controls to validate what was reported and ensure broker/third party SLAs include quality guarantees. Best for Firms Seeking Maximum Control Self-Reporting gives firms complete transparency, control, and governance—ideal for large institutions with diverse products and stringent compliance frameworks. This approach demands investment but supports deep data quality frameworks and audit readiness. Best for Most Mid-to-Large Firms Automated Reporting via Third-Party Vendor offers the most balanced approach, combining broad regulatory coverage with strong data quality tooling and knowledgeable vendor support. It reduces internal maintenance and human resource burdens while supporting scalable, multi-jurisdiction reporting. Final Recommendation Automated Reporting via a Trusted Third-Party Vendor emerges as the most balanced and scalable approach for firms facing diverse products and global regimes if paired with strong internal data governance and oversight. Self-reporting remains the gold standard for control but carries higher cost and complexity, while delegated reporting can be efficient but risks limited visibility and control over data quality. As regulators intensify scrutiny on accuracy, completeness, and auditability of reporting data, firms should prioritise solutions that support: Robust validation and reconciliation End-to-end audit trails Scalability across regimes Clear ownership and control frameworks Combining technology, process, and governance, whether developed in-house or delivered through a vendor, is the foundation for sustainable and compliant transaction reporting. How Complyport Supports Transaction Reporting Complyport’s MAP FinTech Platform is designed to give firms full control and confidence across the entire transaction reporting lifecycle. From data extraction to submission and monitoring, MAP FinTech delivers: End-to-end automation: Streamlined workflows from source data to regulatory submission Advanced data processing: Automated validation, enrichment, and transformation Regulatory agility: full adaptation to evolving global reporting requirements Scalable architecture: Seamless expansion across jurisdictions and regimes Enhanced oversight: Full transparency and monitoring throughout the reporting cycle As a cloud-based platform,

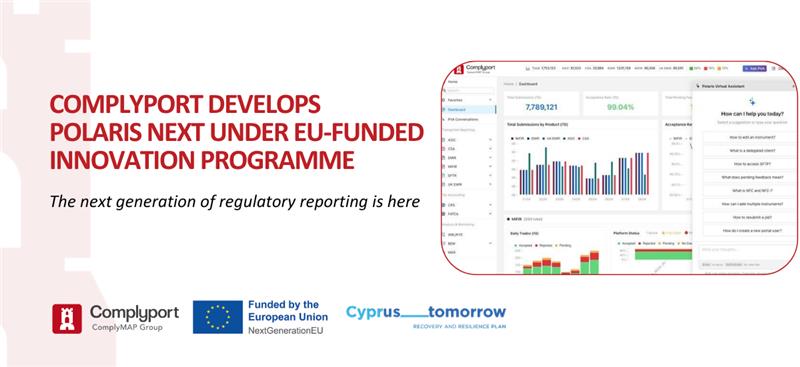

Complyport Unveils Polaris Next: The Next Generation of Regulatory Reporting

We are excited to unveil a major milestone in the evolution of Complyport. After months of focused innovation, we are proud to introduce Polaris Next, the next generation of our regulatory reporting platform, built to redefine performance, intelligence, and user experience for our clients. As we enter the final stages before launch, we are preparing to deliver a step-change upgrade that reflects our long-term vision for the future of regulatory technology. Polaris Next will introduce: Advanced AI-powered capabilities, enabling smarter, faster decision-making and workflows A completely reimagined user experience, designed for clarity, efficiency, and speed Significantly enhanced performance to support scale and growing business demands Strengthened cybersecurity and data protection at the core of the platform This is more than an upgrade; it is a transformation. Polaris Next represents a strategic leap forward, reinforcing our commitment to innovation, resilience, and delivering exceptional value to our clients. This initiative is supported through Project NPD-CAPBLD/0624/0002, under the Cyprus Recovery and Resilience Plan “Cyprus – Tomorrow”, funded by the European Union – NextGenerationEU, through the Research and Innovation Foundation. We look forward to sharing more with you soon and welcoming you to the future of Polaris.

UK MiFIR Transaction Reporting: FCA Reforms and the Road Ahead

How CP25/32 Reshapes Scope, Data Quality, and Implementation Planning The high stakes of Regulatory Divergence Transaction reporting remains one of the most complex and risk-sensitive obligations for UK-regulated firms. The Financial Conduct Authority (FCA) has demonstrated a consistently low tolerance for inaccurate or incomplete data. Even minor technical breaches can trigger intense supervisory scrutiny, costly remediation programmes, and lasting reputational damage UK MiFIR transaction reporting is entering the final phase of regulatory reform. Through Consultation Paper CP25/32, the FCA has proposed changes aimed at simplifying reporting requirements, improving data quality, and refocusing the regime on transactions most relevant to UK market oversight, with final rules expected in the second half of 2026 and a phased implementation thereafter. While the proposals are designed to reduce long-term reporting burden, they will require firms to reassess transaction reporting scope, data models, systems, and controls, particularly as UK requirements continue to diverge from the EU MiFIR framework. Strategic Imperatives for 2026 To mitigate these risks, firms must focus on three core areas throughout this year: Planning is essential: Firms will need to map existing reporting processes to proposed requirements and identify gaps ahead of rule finalisation. Cross-regime consistency matters: Increasing regulatory focus on reducing duplication and improving consistency, where applicable, across reporting regimes under MiFIR, EMIR, and SFTR, requiring a more coordinated data strategy and control framework. Technology change is likely: Updates to reporting logic, data fields, and validation rules are expected to require changes to internal systems and ARM integrations. Regulatory Focus Will Intensify As the FCA moves from consultation to policy finalisation and implementation, delayed planning increases operational and compliance risk, including: Rushed, costly builds Increased error rates during transition Potential enforcement outcomes and data quality failures Early preparation enables firms to influence transitional provisions, test reporting logic thoroughly, and align controls ahead of enforcement spikes. CP25/32 establishes a multi-year reform programme, with key regulatory milestones extending through 2027, as summarised below. UK MiFIR/MiFID Transaction Reporting Timeline Period Date Regulatory milestone November 2024 Nov 2024 FCA publishes Discussion Paper DP24/2 on improving transaction reporting, seeking feedback on potential reform options. February 2025 Feb 2025 DP24/2 discussion period closes. November 2025 21 Nov 2025 FCA publishes Consultation Paper CP25/32, proposing streamlined transaction reporting reforms (including reduced data fields, scope changes, and a shorter back-reporting correction period). Consultation opens. 21 Nov 2025 FCA issues press release highlighting expected cost savings for firms arising from the proposed reforms. Late 2025 Firms begin internal impact assessments and initial planning activities (industry commentary). Early 2026 20 Feb 2026 Consultation on CP25/32 closed on 20 February . Firms now await further detail on transactional planning. Mid – Late 2026 H2 2026 FCA publishes Policy Statement and final rules on transaction reporting reform, as proposed in CP25/32. Late 2026 Start of an anticipated ~18-month implementation period for firms to adapt systems, processes, and controls to the new reporting regime. 2027 Early 2027 (anticipated) Full application of new transaction reporting standards within the FCA’s systems. Throughout 2027 Firms complete implementation of the reformed UK MiFIR transaction reporting regime. Why This Timeline Matters The Preparation Window Is Limited Following the close of the CP25/32 consultation in February 2026, firms have a relatively short period before final rules are published, after which most of the anticipated 18-month implementation window will run. Delayed planning compresses delivery timelines and increases execution risk. Change Is Substantive While the reformed regime is expected to reduce the number of reportable fields, narrow instrument scope, and shorten the historic correction period, these changes will still require material updates to systems, data models, governance frameworks, and reconciliation processes. Regulatory Divergence Continues Post Brexit, the EU and UK transaction regimes began to diverge. In 2024, EU MiFIR expanded the scope of reportable items, and in 2025 ESMA was also consulting on radical changes on reporting (be it EMIR or MiFIR). . Firms operating cross-border cannot rely on a single harmonised solution and will need UK-specific reporting logic, controls, and operational processes. Transitional Provisions Will Be Critical The FCA is expected to issue transitional guidance and supporting Handbook changes following the main Policy Statement and ahead of go-live. Firms will need to monitor these developments closely to ensure implementation plans remain aligned with final requirements. Current Pressures in Transaction Reporting Processes Against this backdrop of ongoing supervisory scrutiny and operational complexity, UK firms continue to face several key pressures in their transaction reporting processes. Data Capture and Quality Data gaps, reconciliation breaks, and complex instrument structures drive manual intervention and increase reporting error risk. Regulatory Change and Divergence Divergence from the EU MiFIR framework means firms cannot simply align UK and EU reporting models, often requiring parallel builds and bespoke compliance logic. Reform Uncertainty Although the reforms are expected to deliver long-term cost savings, they will require system changes, policy updates, vendor coordination, and testing ahead of final rule confirmation and the switching cost may be significant. Enforcement Risk The FCA has demonstrated a low tolerance for inaccurate or incomplete reporting. Even technical breaches can lead to supervisory scrutiny, remediation programmes, and reputational impact. Taken together, these pressures make transaction reporting one of the most complex and risk-sensitive regulatory obligations facing UK-regulated firms. Why Firms Use Specialist Reporting Solutions like Complyport Specialist regulatory reporting platforms are increasingly used by firms to manage the scale, complexity, and change associated with MiFID/MiFIR transaction reporting. Such solutions typically support: Automated data capture, enrichment, and validation to improve consistency and reduce manual effort Regulatory logic aligned to evolving UK MiFIR requirements Strong control frameworks, auditability, and governance support Scalability to accommodate future regulatory change and additional reporting regimes In an environment of ongoing reform and heightened supervisory scrutiny, these capabilities help firms reduce operational risk and support a more controlled and sustainable compliance model. Contact our team of experts for more information or any assistance you may require. By leveraging Complyport’s MiFIR reporting solution, you gain access to a powerful platform and a dedicated team committed to ensuring your compliance success.

FATCA and CRS Reporting 2026: A Guide to Compliance and Automation

For financial institutions, the annual reporting cycle for the Foreign Account Tax Compliance Act (FATCA) and the Common Reporting Standard (CRS) is one of the most operationally demanding compliance exercises of the year. Designed to combat tax evasion and increase transparency, these regulations require banks, investment firms, E-Money institutions, and fiduciary providers to report detailed client data to tax authorities. However, the gap between understanding the regulation and successfully submitting a compliant report is vast. As deadlines approach, institutions must ensure they are not only compliant but efficient. As regulatory reporting obligations expand globally, many institutions are turning to automated CRS and FATCA reporting solutions to manage data collection, validation and submissions more efficiently. The Hidden Challenges of CRS and FATCA Reporting On the surface, FATCA and CRS may appear to be straightforward data submissions. In practice, execution involves navigating a minefield of technical and regulatory hurdles. To ensure a successful submission, firms must tackle: Volume and Detail: A single record often requires the completion of over 65 distinct data fields. Technical Complexity: Transforming internal data into complicated, multi-level XML files that meet strict schema requirements places a heavy burden on IT teams. Regulatory Density: Interpreting the requirements involves navigating over 300 pages of guidance. Jurisdictional Nuances: For globally operating firms, different jurisdictions impose different validation rules, submission formats, and reporting portals. The Cost of Getting It Wrong The risks associated with manual or semi-automated reporting are high. Beyond operational disruption and pressure on internal budgets, the consequences of errors include: Rejected submissions by tax authorities Withholding penalties on specific payments (particularly in cases of false CRS reporting) Potential fines and reputational damage resulting from missed or inaccurate filings Streamline Your Reporting with Complyport At Complyport, we believe regulatory reporting should not drain your resources or your focus. Our highly automated, scalable solution is designed to simplify CRS and FATCA reporting, helping financial institutions manage complex data validation, XML conversion and submissions without sacrificing control of accuracy. Our integrated platform provides a streamlined path to compliant reporting: Data Flexibility: Whether you work with raw data or standard templates, our system ingests your data effortlessly, regardless of volume. Intelligent Validation: Multiple health checks across content and schema automatically identify and filter erroneous entries before submission. Automated XML Conversion: We manage the full conversion to compliant XML files, including automatic separation by tax residency. Global Connectivity: We submit reports to the relevant competent authorities worldwide, ensuring jurisdiction-specific requirements are met consistently. Stay Ahead of the Curve The regulatory landscape is constantly evolving. Complyport maintains ongoing communication with regulators to ensure our system reflects the latest updates and reporting requirements, so your submissions remain accurate year after year. Ready for the Upcoming Deadlines? With reporting deadlines approaching across most participating jurisdictions (see table below), now is the time to secure your reporting process. Avoid last-minute pressure and unnecessary regulatory risk by partnering with a provider that delivers accuracy, efficiency, and confidence. Contact Us Today to learn how our cost-efficient, single-platform solution can simplify your FATCA and CRS obligations. Our solutions empower banks, E-Money institutions, and fiduciary providers to manage not only CRS and FATCA reporting, but a full spectrum of regulatory obligations efficiently and accurately.

EMIR 3-Initial Margin Requirements

EMIR as a set of rules contains many provisions, including but not limited to conduct rules for Central Clearing Counterparties, provisions mandating the clearing of certain OTC derivatives, treatment of derivatives traded on EEA and third country venues, risk mitigation techniques for OTC derivatives uncleared by a CCP, and a reporting obligation. In December 2024 regulation EU 2024/2987 came into effect. The aforesaid regulation amends EMIR in significant ways and has been colloquially dubbed “EMIR 3”. The new rules touch mostly upon the issues of clearing and risk mitigation techniques. It is already widely known that EMIR 3 introduced a requirement for EEA based counterparties to reduce their exposure to non-EEA Clearing Houses by mandating FCs and NFCs+ to open, maintain and actively use accounts with EEA Clearing Houses. One of the least discussed requirements of EMIR 3 however is the requirement placed on NFC+ and FCs with respect to initial margin models for OTC derivatives uncleared by CCPs. Margin RTS vs EMIR 3 : What’s the difference With the so called Margin RTS the EU set requirements regarding the eligibility, management and segregation, the terms for the exchange of margin (mostly initial margin) with respect to OTC derivatives uncleared by a CCP, as well as thresholds/conditions below/under which the Margin RTS can be disapplied. EMIR 3 does not undo the requirements under the Margin RTS, which remain unaffected. EMIR 3 Initial Margin Model – Approval by NCAs Under EMIR 3 FCs as well as NFCs + before implementing a new model for the exchange of initial margin between themselves and their counterparties they will need to apply for authorisation by their home competent authority. If FCs and/or NFCs+ intend to amend a previously authorised model, that triggers a new request for approval by their home NCA. As per EMIR 3 NCAs will have 6 months to approve/reject a new initial margin model, or 3 months to approve/reject a modification to an already approved model. Pro-forma models Many counterparties implement pro-forma initial margin models such as the ISDA Standard Initial Margin Model (ISDA-SIMM), said counterparties will still be required to submit a request for approval from their NCAs, however the process is expected to be expedited by the European Banking Authority which will set-up, maintain and update a centralised database which will validate the said pro-forma models submitted by interested parties. Counterparties that seek approval of their initial margin models based on a pro-forma model will need to include in the application for approval the appropriate references to the EBA’s database. Enhanced supervision of large Investment Firms/Credit institutions EMIR 3 also envisages enhanced supervisory procedures for Investment Firms/Credit Institutions which have a monthly average outstanding notional amount of non-centrally cleared OTC derivatives of at least EUR 750 billion. The supervisory procedures will be co-developed by the European Supervisory Authorities (EBA, ESMA, EIOPA). Exemptions: Single Equity, Index OTC options EMIR 3 ushered a welcomed exception; the new regime allows parties trading Single Equity or Equity Index options to exempt themselves from the requirement of exchanging collateral. MAP FinTech notes that this applies to OTC options uncleared by a CCP. Furthermore, our own subjective view is that considering how plain vanilla option contracts operate and taking into account that collateral is exchanged to hedge against counterparty default risk, we welcome the approach. Opinion by the EBA The EBA has identified early on, that the new ruleset creates a number of issues given that the pro-forma database has yet to be completed, the ESAs have yet to determine the appropriate supervisory mechanisms for NCA’s to scrutinise large investment firms/credit institutions, as well the status of initial margin models already in place prior to EMIR coming into effect. As such the EBA has published an opinion with which it clarifies a few important issues Firms that implemented initial margin models before the entry into force of EMIR 3 are not required to seek approval from their NCA’s to continue using said models. Nevertheless, if firms modify the said models after EMIR 3 came into force they should seek the appropriate approval from their regulators. The format and content of the application that firms need to submit to their NCA’s for approving new IM models or modifying previously approved models. An instruction to the NCAs to deprioritise their supervisory or enforcement actions with respect to large investment firms/credit institutions till after the ESAs finalise their work on the supervisory processes (and they come into effect). An instruction to the NCAs to deprioritise their supervisory or enforcement actions with respect to the applications they receive pursuant to EMIR till the ESAs finalise their guidance or recommendations. Sectoral Impact – EEA based CFD providers Considering that many EEA CFD providers trade with retail clients by and large the initial margin model CFD providers follow is set out in the restrictive measures set by the NCA’s across the EEA(the list is not exhaustive): 3.33% initial margin of the notional value where the underlying is a currency pair comprised of any 2 of the following currencies USD, EUR, JPY, GBP, CAD or CHF. 5% initial margin of the notional value where the underlying is any one of a selected list of Equity Indices (e.g. S&P500, CAC40, DJIA, etc.). 5% initial margin of the notional where the underlying is gold. 5% initial margin of the notional where the underlying is a currency pair comprised of 1 of the currencies referred to in the first bullet point. 10% initial margin of the notional where the underlying is a Commodity Index or an Equity Index not referred to in the second bullet point. 50% initial margin of the notional where the underlying is a crypto asset. 20% initial margin of the notional where the underlying is a single stock. The above restrictive measures on face value are an initial margin model within the meaning of EMIR 3. Considering that the said initial margin model existed before the application of EMIR 3, there is no need for CFD providers to seek approval from their NCAs, regarding the specific case